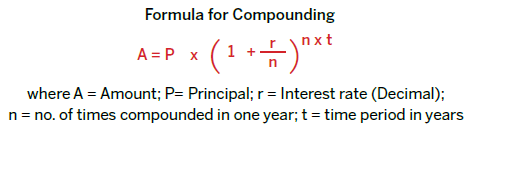

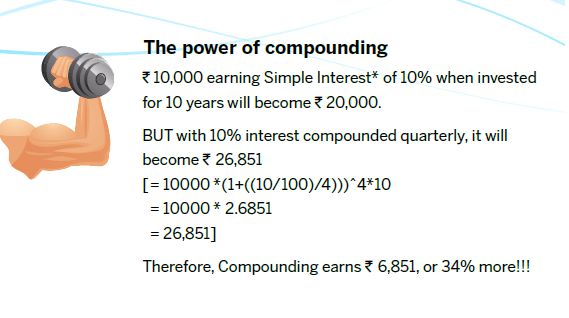

Compounding is also called ‘Interest on Interest’. In compounding, the benefit is that the interest earned is added to the principal and re-invested, therefore earning interest on the principal plus interest.

And when this compounding takes place over a long duration, the return become much higher compared to simple interest*.

An example to explain this:

|

YEAR 1 |

|

|

Principal |

Rs.10,000 |

|

Interest @10% (compounded yearly) |

Rs. 1,000 |

|

Amount at the end of Year 1 |

Rs. 11,000 |

|

YEAR 2 |

|

|

Interest @10% (compounded yearly) on Rs.11,000 (i.e. original Principal Rs. 10,000 + Interest of Rs. 1000) |

Rs.1,100 |

|

Amount at the end of Year 2 |

Rs. 12,100 |

|

YEAR 3 |

|

|

Interest @10% (compounded yearly) on Rs.12,100 (the Amount at the end of Year 2) |

Rs. 1,210 |

|

Amount at the end of Year 3 |

Rs. 13,310 |

*Banks do not offer simple interest rate loan

REMEMBER :

In the long term, huge benefits can accrue from compounding if the money is allowed to remain invested!

Disclaimer : This message is presented as a reading and teaching material with a sincere purpose of making the reader financially literate. It is not intended to influence the reader in making a decision in relation to any particular financial products or services.

Printed by Reserve Bank of India, Financial Inclusion & Development Department.